My mother passed away suddenly over a decade ago. We had no warning or preparation.

I flew cross-country to Florida to attend the funeral that my mother’s husband had arranged. After the funeral, he invited friends and family to their house. It felt surreal seeing my mother’s “stuff” sitting around the house like she had just stepped out for a few minutes and was coming right back. Her hairbrush, hairdryer, magnifying mirror, and makeup were lined up on the bathroom counter. Her closet was filled with clothes and shoes, just as she had left it.

I opened up my mother’s jewelry box. I suppose it not only contained her jewelry, but also my grandmother’s jewelry. I was traumatized and in shock so I asked my mother’s husband and her first cousin (who lived locally and was a good friend to my mother) to work together and figure out what to do with her jewelry and all her other belongings. For sentimental reasons I took two necklaces and one pair of earrings I remembered seeing my mother wear often over the years, and left everything else in the jewelry box.

I never saw that jewelry box again.

I have no idea if my mother owned any jewelry of significant value, and if she did, I wouldn’t have worn it anyway. Her cocktail rings, diamond stud earrings, long necklaces, and lapel pins had no place in my contemporary, minimalist wardrobe. Let’s be honest — jewelry you inherit from a person you love dearly may not be your style. I don’t see many women besides U.S. House Speaker Nancy Pelosi wearing pearls these days. However, just because my wardrobe may not have benefitted from those pieces doesn’t mean they didn’t hold value. Many people today are finding that selling inherited jewelry can help them pay tribute to their loved ones and benefit their own personal finances.

Maybe you’ve come into a recent inheritance of valuable jewelry or watches that just don’t fit your lifestyle. Or you’ve recently come to the conclusion that your jewelry collection is not so you anymore. In that case, you may want to consider selling these items. A recent Worthy client sold a Rolex watch for $2,019 and a Cartier watch for $2,700. The seller of these watches realized she could put close to $5,000 to work instead of leaving the value locked up in pieces that tell time. I hope the seller invested that money for her future.

If you inherited a box full of jewelry, how many times would you wear an expensive necklace that is befitting for a ballroom gown or a gold watch that would look sharp paired with a shoulder-padded power pantsuit? Would you pass on an antique pin to your daughter to wear on her lapel? Are there any clothes made for children, teens and young adults anymore that even have lapels?

What about the jewelry you’ve been gathering over the years? Many of the items in your jewelry box might not fit today’s casual lifestyle and athleisure-filled closets.

If you are the creative type you could redesign the jewelry. If you are financially secure you could donate it. Or you could sell it and use the cash to buy the jewelry you want. But the reality is that most women are not financially secure. If you fit this category, it is certainly worth your time to get a box of inherited jewelry looked at by an expert, a service Worthy offers at no cost or inconvenience to you.

What would you do with that money?

While it might be tempting to put it towards a fabulous vacation, a new car, or a jacuzzi, I have some more practical suggestions:

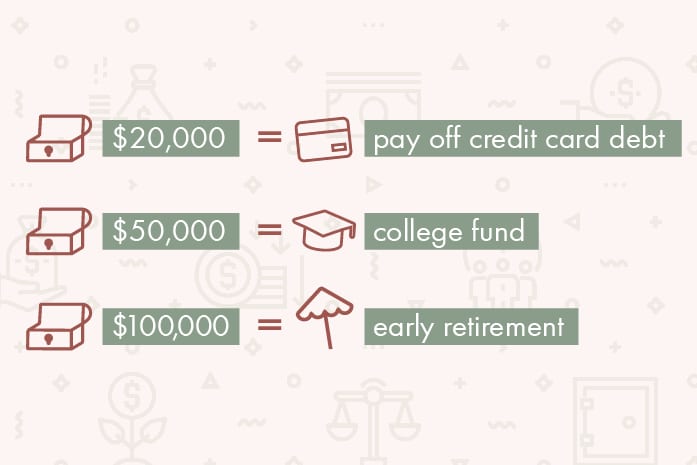

If you had $20,000 in credit card debt and the credit card company charged 20% in annual interest, even if you consistently made a $400 payment each month, it would take you more than 30 years to pay off your debt! Over that time period, you would have paid more than $70,000 in interest on $20,000 worth of purchases. Credit card debt can be a black hole from which you can’t escape. If you receive a lump sum of cash, paying off debt is a great idea.

If you were to front-load a 529 college savings account with $50,000 for an 8-year-old child, assuming the account returned about 7% per year, you could end up with $100,000 when your child graduates from high school. That money could be withdrawn tax-free to pay for tuition, housing, books and fees. While it might not pay for four years at a private university, it would make quite a dent and leave your child with less to pay in student loans.

If you were to generate $100,000 by selling your jewelry, that money could be invested to help you retire early. If you were able to invest $100,000 in an account that generated a 5% annual after-tax return for 20 years, you would end up with over $250,000. That could pay for your living expenses for a number of years.

Become one of those women who are turning jewelry into something more valuable. Pay off debt, invest in your child’s future, or shorten the number of years you need to work.

Interested in learning more ways to become more financially secure and empowered? Sign up for my free monthly newsletter or request a consultation at www.TheOptionsLady.com.

Disclaimer: Investing carries risk. The figures referenced in this article are for educational purposes only. Before investing, consult with a financial advisor who is familiar with your individual situation.

©2011-2026 Worthy, Inc. All rights reserved.

Worthy, Inc. operates from 25 West 45th St., 2nd Floor, New York, NY 10036